.png)

What is carrier liability insurance? This friendly guide explains your coverage, limits, and how to protect your freight from loss or damage.

Let's get one thing straight right from the start: carrier liability insurance is the absolute bare-minimum coverage a freight carrier is legally required to have. It holds them financially responsible if your goods are lost or damaged, but—and this is a big "but"—only up to a very limited amount.

It's a huge mistake to think of it as full-value insurance. More often than not, it pays out based on the weight of your cargo, not what it's actually worth, and only if you can prove the carrier was negligent.

Have you ever hired a moving company? You probably remember them offering a basic, included insurance plan. It's nice to have, but you know it won't come close to covering the full cost of your big-screen TV or antique dresser if something goes wrong. Carrier liability insurance is pretty much the same deal, just for the freight world.

Think of it as a safety net with some pretty big holes. Its real purpose is just to set a baseline for the carrier's responsibility during transit. The most common and costly mistake shippers make is assuming this basic coverage fully protects their investment. It absolutely does not.

Here's the kicker with carrier liability insurance: it all hinges on the concept of negligence. For a claim to even be considered, you, the shipper, have to prove that the loss or damage was a direct result of the carrier messing up or failing to take proper care.

This means if a tornado, flood, or some other "Act of God" destroys the shipment, your claim is probably getting denied. The burden of proof is 100% on you.

Key Takeaway: Carrier liability isn't an automatic payout. It only kicks in if you can prove the carrier was at fault, which makes the whole claims process a lot trickier than with other types of insurance.

Forget what you know about typical insurance policies that cover an item's declared value. Carrier liability payouts are almost always figured out using a set formula, and it's usually based on the weight of the damaged goods, not their real-world price tag.

For instance, the limit might be a measly $0.50 per pound. This is where shippers can get into serious financial trouble.

This per-pound limit is the single most important detail to understand. It’s exactly why relying only on this basic coverage is a massive gamble, especially if your products are valuable. Once you know your shipment’s value blows past these tiny limits, it's time to get a quote that includes real protection.

Let's be honest—diving into the fine print of an insurance policy is nobody's idea of a good time. But when it comes to carrier liability insurance, this is precisely where the most important, and often costly, details are hiding. Understanding what’s covered, what isn't, and for how much is the only way to protect yourself from a nasty financial shock when a claim arises.

The biggest "gotcha" for most shippers is how the coverage limit is calculated. It’s almost never based on the actual value of your goods. Instead, it’s typically a simple dollar-per-pound formula, which can create a massive gap between what your cargo is worth and what you'll get paid if something goes wrong.

Let’s put this into perspective with a real-world example. Say you're shipping a pallet of valuable, custom-printed circuit boards.

If that entire shipment is lost or destroyed due to proven carrier negligence, the absolute maximum payout you could receive is a mere $500. That’s it. You're left on the hook for a staggering $49,500 loss. On the flip side, if you were shipping 500 pounds of scrap metal valued at $200, you’d be fully covered. This stark contrast shows just how risky it is to rely only on basic carrier liability for anything of value.

On top of the frustratingly low payout limits, every policy has a list of exclusions. Think of these as the specific situations where the carrier can legally walk away without paying a dime, even if your goods are completely ruined. These are the loopholes that can sink your claim before it even gets started.

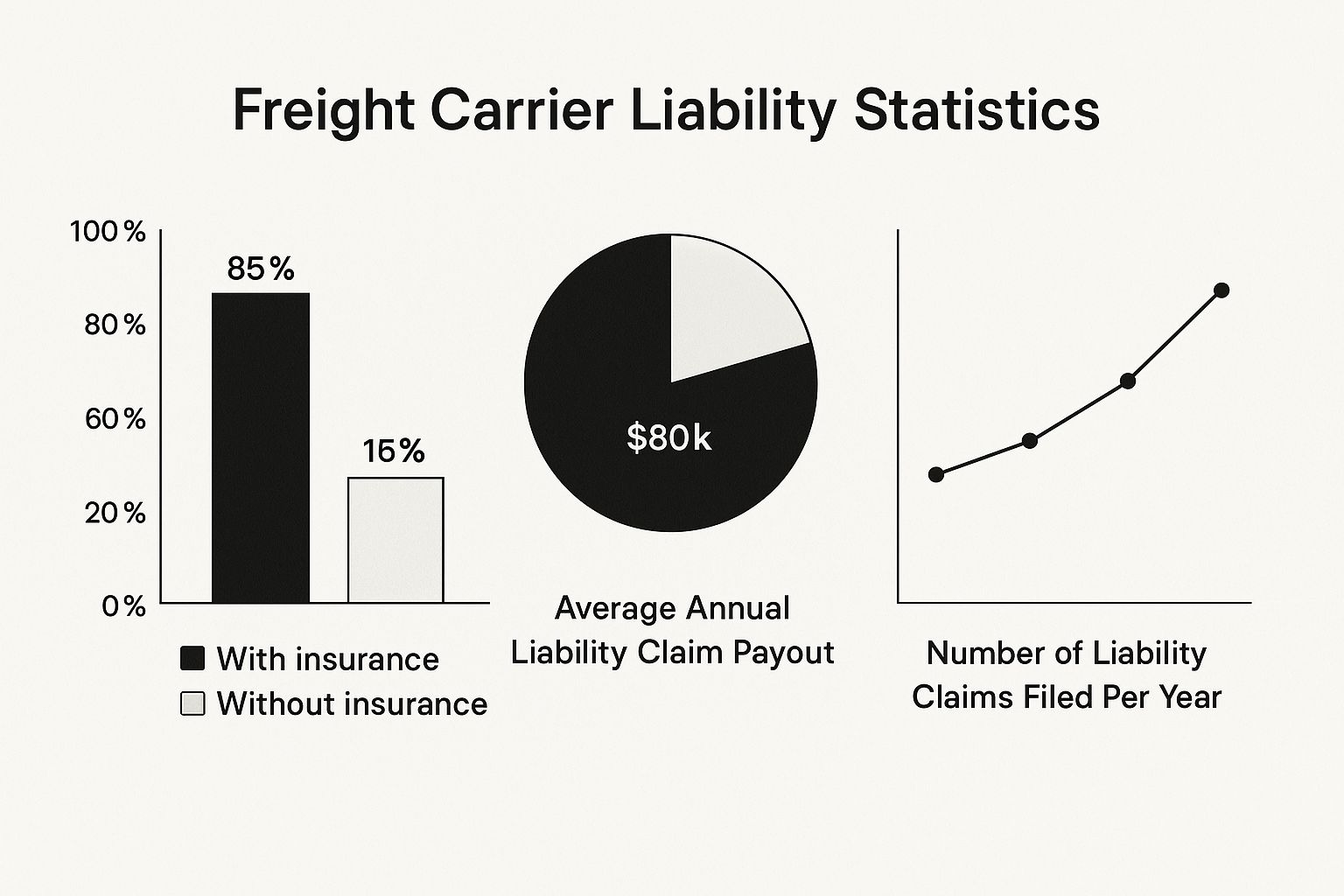

This chart gives you a quick snapshot of why understanding these details is so critical in the real world of freight.

As you can see, claims are a frequent and expensive part of the business. Knowing the rules of the game is your best defense.

The table below breaks down some of the most common scenarios. It's a quick cheat sheet for understanding when you're likely covered versus when you're on your own.

Understanding these exclusions is the first step in building a smarter shipping strategy. It’s not just about what the carrier will do; it’s about what they don’t have to do.

Here’s a quick rundown of the most common reasons your claim might be denied:

Shipper's Tip: Always, always, always take photos of your freight after it's been packaged and palletized but before the carrier picks it up. This simple step can be your best evidence to fight a claim denial based on "improper packaging."

Navigating these risks proactively is key. To get ahead of these issues, take a look at our complete guide on transportation risk management for practical strategies to protect your shipments from the start.

This is one of the most critical distinctions in the shipping world, and confusing the two is an easy—and often costly—mistake. Let’s clear it up with an analogy we've all run into.

Think about the last time you rented a car. The rental company gives you basic, built-in liability coverage. That protects them if something goes wrong, but it offers next to nothing for you or the vehicle. For real peace of mind, you have to buy the optional, full-coverage collision damage waiver.

It's the exact same principle in freight:

That’s the core difference. Carrier liability is the carrier's safety net, with strict limits and lots of loopholes. Freight insurance is your safety net, designed to protect the full value of your products.

Freight insurance, also known as cargo insurance, is a completely different beast. It's a first-party policy that you, the shipper, purchase and control. It exists for one reason: to fill the massive gaps that carrier liability leaves wide open.

Its goal is simple: to make you financially whole if your goods are lost or damaged on the road, no matter who was at fault.

Think of it as a proactive move. Carrier liability is reactive—it forces you to go after the carrier and prove they messed up. Freight insurance provides much broader "all-risk" coverage, protecting you from a whole host of problems that carrier liability won't touch, like storms or other "Acts of God."

The Shipper's Advantage: With freight insurance, you're dealing with your insurance provider, not arguing with the carrier. This almost always means a faster, simpler, and more successful claims process.

Once you realize your cargo's value far exceeds the carrier's basic limits, getting the right freight insurance is the only logical next step.

Let’s put these two side-by-side. Seeing the differences laid out clearly shows why relying only on carrier liability is a huge financial gamble. Making the right choice here directly protects your bottom line and keeps your business running smoothly.

Smart insurance choices are a cornerstone of any solid logistics strategy. For more on this, see our guide on how to improve supply chain efficiency and learn how risk management fits into the bigger picture. At the end of the day, freight insurance is your business's personal financial safeguard, making sure one bad shipment doesn't turn into a catastrophic loss.

That sinking feeling when you discover your freight is damaged or missing is something no one wants to experience. Filing a claim can feel like gearing up for a fight, but it doesn't have to be a legal nightmare. The trick is to be methodical, quick, and prepared—because when it comes to a claim, the burden of proof is squarely on your shoulders.

Believe it or not, your success in the claims game starts the second that truck backs up to your dock, long before you’ve even spotted a problem. Those first few moments are absolutely critical. A quick, distracted signature on the delivery paperwork can accidentally sign away your right to a claim, so a little diligence up front is your best defense.

Think of it like this: you're building a case file for an investigator. The clearer and more compelling your evidence is, the better your odds of getting paid. Your goal is to leave no doubt that the damage happened while the carrier was responsible for your goods.

Follow these steps to the letter to protect your business.

Inspect Before You Sign: This is the absolute golden rule of receiving freight. Before you put pen to paper on the Proof of Delivery (POD) or Bill of Lading (BOL), give that shipment a thorough once-over. Look for any visible red flags on the packaging—crushed corners, tears, water stains, anything out of the ordinary. If you can, pop open the crates and check the goods themselves.

Document Everything on the Delivery Receipt: Find something wrong? Note it on the delivery receipt before the driver leaves. And be specific. "Damaged" is too vague. Instead, write something like, "Box 3 of 5 crushed on top right corner, contents exposed." This creates an official, time-stamped record that the damage was there on arrival.

Take Detailed Photographs: In a freight claim, a picture is truly worth a thousand words—or in this case, a thousand dollars. Snap photos of the damaged packaging from a few different angles, get close-ups of the product damage, and take a wider shot showing the damaged items on the pallet. Good lighting and clear focus are your friends here.

Once you've noted the damage, the clock starts ticking. You have to move fast to file your formal claim. Carrier liability insurance policies have very strict deadlines. You often have just a few days to report the problem and a hard nine-month window to submit the complete claim file.

To build a rock-solid claim, you'll need to pull together a few key documents. Having them organized and ready to go shows the carrier you're serious and helps avoid any unnecessary back-and-forth.

Your claim package should always include:

A common rookie mistake is to only claim the wholesale cost of the damaged product. Don't forget to include the freight charges and any inspection fees you paid as part of your total financial loss.

From there, the carrier will launch an investigation, which can take anywhere from 30 to 120 days. They'll review all the evidence to decide if their negligence was the cause. A well-documented, airtight claim makes it much, much harder for them to say no.

If you're shipping anything of significant value, the financial hit from a denied or limited payout can be huge. The best strategy is always to protect your shipment from the get-go.

Ever look at a freight bill and wonder why the costs seem to ebb and flow? It’s not just about fuel prices or driver availability. The cost of your shipment is directly connected to a web of larger market forces, particularly those driving up the price of carrier liability insurance.

Understanding these trends is like having an inside look at the industry. It helps you anticipate budget changes and make smarter logistics decisions. You’re not just paying for a service; you're navigating a complex and constantly shifting global market.

Two of the biggest factors pushing insurance premiums skyward are "social inflation" and "nuclear verdicts." These aren't just buzzwords; they represent a real shift in the legal landscape that directly impacts every carrier on the road.

Social inflation describes a growing trend where juries are more willing to side with plaintiffs, awarding massive settlements in liability cases. This is often fueled by a general mistrust of large corporations and a desire to hold companies accountable.

This sentiment has led to an explosion of nuclear verdicts—jury awards that soar past the $10 million mark. When a trucking company gets hit with a verdict that big, the shockwaves ripple across the entire insurance industry. Insurers have to pay out enormous sums, which forces them to raise premiums for all carriers to cover their increased risk.

Ultimately, these higher operational costs for carriers get passed down the line and show up in the shipping rates you pay.

The insurance market isn't a monolith; it behaves differently depending on where you are in the world. This is especially true when you compare the United States and Europe. The U.S. legal system, with its tendency for high-stakes litigation and massive jury awards, creates a much more volatile and expensive insurance environment for carriers.

Due to these pressures, the U.S. commercial auto insurance sector has faced significant underwriting losses. Insurers are responding by tightening their belts with higher premiums, more restrictive policy terms, and smaller coverage limits to manage their exposure.

In contrast, many European countries have more predictable legal systems with caps on damages, resulting in a more stable and affordable insurance market for their carriers. This regional difference can influence international shipping costs and carrier availability. A carrier operating in the U.S., for example, will almost certainly have higher insurance overhead than one operating exclusively in Germany.

These dynamics show how persistent pressures are affecting carrier liability insurance costs and availability. According to recent market analysis, even as some global insurance rates soften, casualty lines like commercial auto insurance continue to face upward pricing pressure, particularly in the United States. You can explore the full 2025 insurance market report to see a detailed breakdown of these trends. This insight is key to understanding the full picture of your freight costs.

Let’s be honest: the best claim is the one you never have to file. While carrier liability insurance is your safety net for when things go sideways, the real win is preventing problems from ever happening in the first place. A little foresight can save you a world of time, money, and stress.

Smart shipping isn't just about what happens on the road; it starts right in your warehouse with how you prep your freight. Taking a few extra minutes to properly secure your cargo is hands-down the most powerful thing you can do to avoid damage.

Think of your packaging as armor. Flimsy boxes, wobbly pallets, or a lack of proper cushioning are like sending your products into battle unprotected. Carriers are quick to deny claims based on insufficient packaging, so this is one area where you can't afford to cut corners.

Here’s how to build a solid defense:

Getting these fundamentals right is your first line of defense. To take a more comprehensive look at safeguarding your entire logistics process, check out our guide on supply chain risk management.

Beyond the physical prep, accurate paperwork and modern tools add another crucial layer of protection. Something as simple as an incorrect freight classification can cause billing headaches and handling mistakes down the line.

Getting the National Motor Freight Classification (NMFC) code right from the start ensures your shipment is priced and handled correctly. This small detail helps you sidestep unexpected issues that could put your freight at risk.

It's also worth noting that the global insurance market is always in flux. For example, in early 2025, the U.S. insurance market saw tighter conditions and more intense underwriting scrutiny than in other parts of the world. At the same time, new tech like telematics is changing how insurers evaluate risk. You can learn more about these global insurance market trends to stay informed.

By shipping smarter and staying proactive, you put your business in the best possible position to handle whatever the road throws at you.

Let's be honest, carrier liability insurance can feel like a tangled mess of rules and exceptions. If you're scratching your head, you're not alone. We've pulled together some of the most common questions shippers ask to give you the straight scoop and help you navigate the process with a lot more confidence.

Not every single time, but if your goods are valuable or delicate, it’s a very smart move. Think of it this way: the carrier’s basic liability only covers a set amount per pound. You need to ask yourself if that amount comes anywhere close to the actual value of what you're shipping.

If there's a big gap between what the carrier will pay and what your stuff is actually worth, freight insurance is your safety net. It's designed to protect your real financial investment and kicks in for a much wider range of scenarios that basic liability simply ignores.

This is one area where you absolutely cannot drag your feet. The deadlines are iron-clad. While the exact rules can differ from one carrier to the next, you often have a shockingly short window—sometimes just 5 to 9 days—to let them know something is wrong.

Once you’ve given that initial notice, the clock starts ticking on filing the full, formal claim, which is usually due within nine months. Your Bill of Lading (BOL) is your guide here; it will spell out the specific time limits for your shipment.

Pro Tip: Don't put this off. The moment you spot damage, document everything and report it. Waiting, even a day, can mean forfeiting your right to file a claim, and that’s a costly lesson to learn.

While both are based on the same idea—that the carrier is responsible for damage caused by their negligence—the way coverage is calculated can be worlds apart. It's a critical detail you need to nail down before your freight ever leaves the dock.

The bottom line is, never assume the coverage is the same. Verifying the specific liability limits for every single shipment, whether it's LTL or FTL, is a non-negotiable step in smart risk management.

At FreightQuotesNow, we make this easy. We connect you with carriers who have the right coverage for your specific freight, giving you peace of mind from pickup to delivery. Get an instant quote today and ship with confidence.